Minimum Alternate Tax Mat Pdf

Minimum Alternate Tax

Minimum Alternate Tax Tax Credit Tax Deduction

Mat Vs Amt Minimum Alternate Tax And Alternative Minimum Tax Vakilsearch

Title Minimum Alternate Tax Mat Author Ca Kamal Garg Publisher Bharat Law House 6th Edition 2017 Type Paperback Vorabookh Vora Books Bookstore

Minimum Alternate Tax In India A Comparative Analysis Of Provisions Under Income Tax Act And Direct Tax Code

Guide To Minimum Alternate Tax For Ind As Compliant Companies

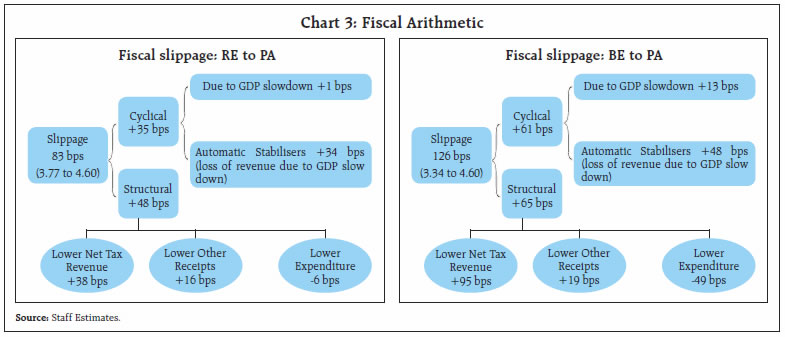

15th june 2017 1.

Minimum alternate tax mat pdf. Understanding the concept of liability to pay minimum alternate tax mat and alternate minimum tax amt and various provisions like book profit dividends paid or proposed depreciation deferred tax income of foreign company etc. Minimum alternate tax mat markets and mayhem. Mat and amt mat stands for minimum alternate tax and amt stands for alternate minimum tax. Initially the concept of mat was introduced for companies and progressively it has been made applicable to all other taxpayers in the form of amt.

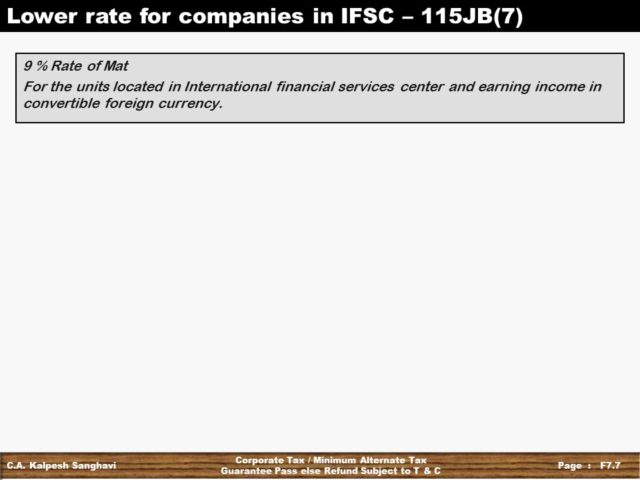

Mat is levied at the lower rate of 9 plus surcharge and cess as applicable for companies that are a unit of an international financial services centre and derive their income solely in. In this part you can gain knowledge about various provisions relating to mat and amt. It was introduced in the year 1987 and. For provisions relating to amt refer tutorial on mat amt in tutorial section.

Introduction as the book profit based on ind as compliant financial statement is likely to be different from the book profit based on existing indian gaap the cbdt constituted a committee in june 2015 for suggesting. This tax is computed using a separate charging section altogether. Faced with requests for clarity the mat provisions were amended in 2015 to exempt fpis from paying mat on capital gains. In india mat is levied under section 115jb of the income tax act 1961.

With mat companies have to pay up a minimum amount of tax to the government. Over the last year foreign portfolio investors fpis have been asked to pay mat on the past capital gains. Year it is a new tax controversy. In the case of a non corporate taxpayer to whom the provisions of alternate minimum tax amt applies tax payable cannot be less than 18 5 hec of adjusted total income computed as per section 115jc.

For fy 2019 20 tax payable is computed at 15 previously 18 5 on book profit plus applicable cess and surcharge.

All About Alternate Minimum Tax Amt Section 115jc

Https Www2 Deloitte Com Content Dam Deloitte In Documents Tax In Tax Minimum Alternate Companies Noexp Pdf

Https Papers Ssrn Com Sol3 Delivery Cfm Ssrn Id1759907 Code1612178 Pdf Abstractid 1759907 Mirid 1

Ca Final Question Bank Dt Minimum Alternate Tax Mat

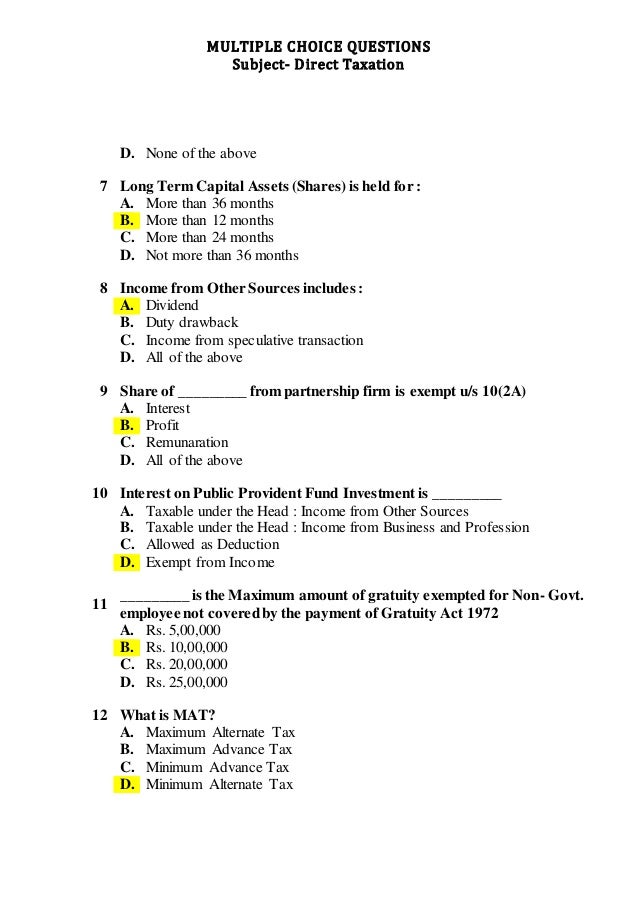

Multiple Choice Questions On Direct Taxation

Minimum Alternate Tax Mat Section 115jb

Explained What Is Minimum Alternate Tax Or Mat

Memory Technique Minimum Alternate Tax Section 115jb May Nov 2019 Attempt Youtube

Mat Vs Amt Minimum Alternate Tax Alternate Minimum Tax Indiafilings

Incometaxindiaefiling Gov In Efiling Portal Staticpdf Response Defective Return Pdf Income Tax Math Portal

What Is Minimum Alternate Tax Mat News Budget 2020 News Mat Calculation

What Are The Recommendations For Union Budget 2019 Suggested By Aiftp

Pdf Goods And Service Tax A Detailed Explanation With Examples Taxguru In Goods And Service Tax Goods Service Tax Detailed Explanation Examples Html Thirupal Gandhudi Academia Edu

Difference Between Mb Ib Investment Banking Banks

Calculation Of Mat Credit Applicability Of Minimum Alternate Tax

Pdf Algorithm For Calculating Corporate Marginal Tax Rate Using Monte Carlo Simulation

Minimum Alternate Tax For Companies Indiafilings

Pdf Budget Terminology Rose M Academia Edu

Government Notifies The Direct Tax Vivad Se Vishwas Rules 2020 And Corresponding Form

Https Www Singtel Com Content Dam Singtel Investorrelations Stockexchange 2020 Balrelease 20200730 Pdf

Download Pdf Ca Final Direct Tax Important Questions Nov 2019 Income Tax

Current Income Tax Rates For Fy 2019 20 Ay 2020 21 Sag Infotech

Corporate Tax In India Overview Rates Tax Liability

Pdf Emerging Trend In Indian Direct Taxation An Analysis Of Income Computation And Disclosure Standards

Https Www2 Deloitte Com Content Dam Deloitte In Documents Tax In Tax Unionbudget2019 Publication Noexp Pdf

Panel On Direct Tax Code Drishti Ias

Vivad Se Vishwas Scheme

Penalties Under Income Tax Act 1961

Insights Into Editorial Secular In Spirit And In Letter Mindmaps On Current Issues Insightsias

India No Permanent Establishment Found Kpmg United States

Reserve Bank Of India Rbi Bulletin

T N Manoharan

Yojana Magazine Analysis March 2020 Free Pdf Download

Https Ieeexplore Ieee Org Iel7 6287639 8600701 08694987 Pdf

Https Www Protact In Application Public Uploads Cms 762 1806 Mat Amt Provisions Under Income Tax Pdf

Indian Taxation System For Banking Ssc Gk Notes In Pdf

Https Www Taxmann Com Bookstore Catalogues Taxmann 20laws 20v16p7 It 20act 20 Pgs 201 20 Webjuly2019 Pdf

Https Www2 Deloitte Com Content Dam Deloitte Ie Documents Financialservices Investmentmanagement Ie 2015 1 10 15 Tax Investment Management Pdf

Https Papers Ssrn Com Sol3 Delivery Cfm Ssrn Id3425355 Code3366507 Pdf Abstractid 3425355 Mirid 1

Https Www Pwc In Assets Pdfs Publications 2017 Pwc Reportingperspectives October 2017 Pdf

Pin By Meri Pustak On Academic Books In India Pinterest

Pdf Challenges Of Direct Tax Code 2010 Over Income Tax Act 1961

Corporate Income Tax Insightsias